The Complete Guide to Credit Scores

Complete Guide to Credit Scores

Your credit score is one of the most important numbers in your financial life. It influences whether you’re approved for a mortgage, qualify for a low-interest auto loan, receive favorable credit card offers, or even rent an apartment.

The good news is that credit scores aren’t random. They’re calculated using predictable factors, which means you have the ability to improve yours over time with consistent financial habits.

Whether you’re starting from scratch, rebuilding after financial setbacks, or trying to reach an excellent score, this guide explains everything you need to know.

Quick Credit Score Reference

| Credit Score | Rating | What It Generally Means |

|---|---|---|

| 300–579 | Poor | Difficult to qualify for most loans and credit cards |

| 580–669 | Fair | May qualify, but often with higher interest rates |

| 670–739 | Good | Eligible for many lending products |

| 740–799 | Very Good | Better loan terms and lower interest rates |

| 800–850 | Exceptional | Access to the most competitive lending offers |

Editor’s Recommendation: Don’t focus on achieving a perfect 850. For many lenders, a score of 760 or higher is enough to qualify for their best available rates.

What Is a Credit Score?

A credit score is a three-digit number that estimates how likely you are to repay borrowed money based on your credit history.

Lenders use this score to evaluate risk before approving applications for:

- Credit cards

- Mortgages

- Auto loans

- Personal loans

- Student loans

- Apartment rentals

- Some insurance products

- Certain employment screenings where permitted by law

A higher score generally signals responsible credit management and lower lending risk.

Why Credit Scores Matter

Your credit score affects far more than loan approvals.

Strong credit can help you:

- Qualify for lower interest rates

- Save thousands of dollars over the life of a loan

- Receive higher credit limits

- Obtain better credit card rewards

- Rent an apartment more easily

- Reduce security deposits

- Increase financing options

Poor credit may lead to:

- Higher interest rates

- Loan denials

- Lower credit limits

- Larger deposits

- More restrictive lending terms

How Better Credit Can Save You Thousands

Improving your credit score isn’t simply about getting approved for financing—it’s about paying less for the money you borrow.

| Credit Score Range | Typical Interest Rate Trend | Long-Term Cost |

| Poor (300–579) | Highest | Highest borrowing costs |

| Fair (580–669) | Higher than average | Thousands more paid in interest |

| Good (670–739) | Competitive | Lower monthly payments |

| Very Good (740–799) | Better | Significant long-term savings |

| Exceptional (800–850) | Best available from many lenders | Lowest borrowing costs |

Even a slightly lower interest rate on a mortgage or auto loan can save thousands of dollars over the life of the loan.

The Two Most Common Credit Scores

Although many people think they have one credit score, you likely have several.

FICO Score

The FICO Score is the scoring model used by many lenders when making lending decisions.

VantageScore

VantageScore was developed by the three major credit bureaus and is commonly used by credit monitoring services and some lenders.

Both models evaluate similar information but use different formulas, so your scores may differ.

The Five Factors That Affect Your Credit Score

1. Payment History

Importance: Very High

Payment history measures whether you’ve paid your accounts on time.

Positive examples include:

- On-time mortgage payments

- Credit card payments

- Auto loan payments

- Personal loan payments

Negative items include:

- Late payments

- Collections

- Charge-offs

- Bankruptcies

- Foreclosures

Even one late payment can affect your score.

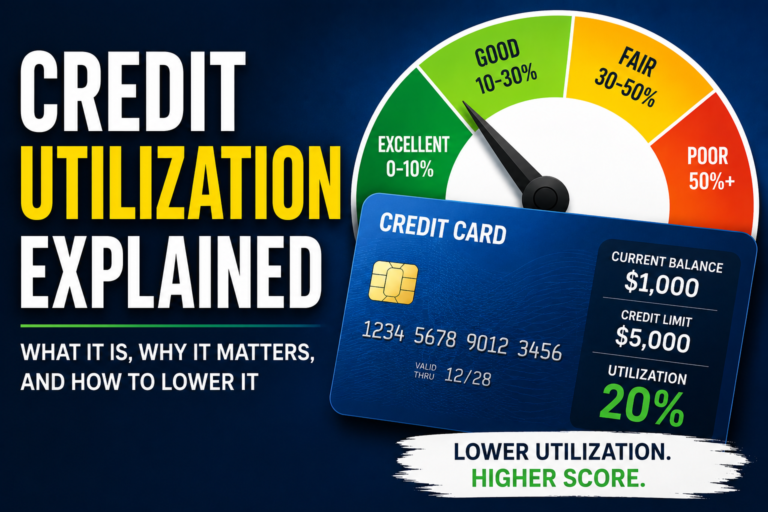

2. Credit Utilization

Importance: High

Credit utilization measures how much revolving credit you’re using compared to your available credit.

Example:

- Credit Limit: $10,000

- Current Balance: $2,000

- Utilization: 20%

General guidelines:

- Under 30% is considered healthy.

- Under 10% is even better.

3. Length of Credit History

Longer credit histories generally help because lenders have more information about your borrowing habits.

This includes:

- Age of oldest account

- Average account age

- Age of newest account

4. New Credit

Opening several new accounts within a short period may temporarily reduce your score because of hard inquiries.

Only apply for credit when you actually need it.

5. Credit Mix

Having experience managing different types of credit can be beneficial.

Examples include:

- Credit cards

- Mortgages

- Auto loans

- Student loans

- Personal loans

Never open unnecessary accounts simply to improve your credit mix.

What Does Not Affect Your Credit Score?

Contrary to popular belief, these factors generally do not directly affect your credit score:

- Income

- Savings account balance

- Checking account balance

- Occupation

- Education

- Marital status

- Race

- Gender

What Is Considered a Good Credit Score?

Although lenders vary, these ranges are commonly used:

- Poor: 300–579

- Fair: 580–669

- Good: 670–739

- Very Good: 740–799

- Exceptional: 800–850

Credit Scores by Financial Goal

Most people don’t want a better credit score just to have a higher number—they want to accomplish important financial goals.

| Financial Goal | Recommended Credit Score |

| Rent an Apartment | 650+ |

| Finance a Vehicle | 660+ |

| Buy a Home | 620–760+ depending on loan type |

| Refinance a Mortgage | 700+ |

| Premium Credit Cards | 700–740+ |

| Business Financing | 680–740+ |

| Best Available Loan Rates | 760+ |

Remember that lenders also evaluate your income, debt-to-income ratio, employment history, and assets.

How to Improve Your Credit Score

Improving your score requires consistent habits rather than quick fixes.

Pay Every Bill on Time

Your payment history is one of the biggest scoring factors.

Lower Credit Card Balances

Reducing balances often produces one of the quickest improvements.

Keep Utilization Low

Aim to use less than 30% of your available credit, with under 10% being even better.

Avoid Unnecessary Credit Applications

Too many hard inquiries within a short period may temporarily lower your score.

Review Your Credit Reports

Check for reporting errors and signs of identity theft.

Keep Older Accounts Open

Older accounts help strengthen the average age of your credit history.

Continue Building Positive History

Time and consistency are your greatest allies.

Credit Score Improvement Roadmap

If you’re unsure where to begin, follow this roadmap.

Step 1: Never miss a payment.

↓

Step 2: Pay down revolving credit card balances.

↓

Step 3: Keep utilization below 30%.

↓

Step 4: Review your credit reports for errors.

↓

Step 5: Avoid unnecessary hard inquiries.

↓

Step 6: Continue building positive payment history.

↓

Step 7: Monitor your progress every month.

Improving your credit isn’t about shortcuts. It’s about consistently demonstrating responsible financial behavior.

How Long Does It Take to Improve a Credit Score?

Everyone’s situation is different, but improvements often happen gradually.

Credit Score Improvement Timeline

| Time | What You May See |

| First 30 Days | Lower balances begin reporting |

| 60 Days | Consistent on-time payments accumulate |

| 90 Days | Measurable improvement may begin appearing |

| 6 Months | Positive payment history continues building |

| 12 Months | Many borrowers experience meaningful long-term improvement |

Patience and consistency usually outperform quick fixes.

What Happens to Your Credit Score If…

Many financial decisions affect your score differently.

| Action | Possible Impact |

| Miss one payment | May significantly lower your score |

| Pay off a credit card | Often improves utilization |

| Max out a credit card | May lower your score |

| Close your oldest credit card | Could reduce available credit and affect account age |

| Apply for new credit | Small temporary decrease possible |

| Become an authorized user | May improve your score if the account has positive history |

| Pay a collection account | Impact varies by scoring model |

| File bankruptcy | Major long-term negative impact |

Every credit profile is unique, so individual results vary.

Common Credit Score Mistakes

Avoid these common mistakes:

- Missing payment due dates

- Carrying high balances

- Closing your oldest account

- Applying for multiple credit cards

- Ignoring credit report errors

- Cosigning loans without understanding the risks

- Paying only the minimum payment for extended periods

Credit Score Mistakes by Age

In Your 20s

- Missing first payments

- Maxing out starter credit cards

- Opening too many retail cards

- Ignoring student loans

In Your 30s

- Carrying high balances

- Financing multiple major purchases

- Missing payments because of growing expenses

- Opening several accounts at once

In Your 40s and Beyond

- Closing older accounts

- Cosigning loans for family members

- Carrying unnecessary debt

- Not monitoring credit reports for fraud

Regardless of your age, paying on time and managing debt responsibly remain the foundation of excellent credit.

How Often Should You Check Your Credit Score?

Checking your own score is typically considered a soft inquiry and generally does not lower your credit score.

Review your score monthly to:

- Detect fraud early

- Monitor progress

- Track utilization

- Catch reporting errors

Credit Score Improvement Checklist

Use this checklist throughout the year.

- Pay every bill on time.

- Keep utilization below 30%.

- Review your credit reports.

- Dispute inaccurate information.

- Avoid unnecessary hard inquiries.

- Keep older accounts open when practical.

- Build an emergency fund.

- Monitor your score monthly.

Your Financial Tool

Your credit score is one of the most valuable financial tools you have. While it doesn’t define your financial future, it influences many opportunities—from buying a home and financing a vehicle to qualifying for lower interest rates and premium financial products.

The encouraging news is that credit scores are built through consistent habits. Paying bills on time, managing debt responsibly, keeping credit card balances low, and regularly reviewing your credit reports can lead to meaningful improvements over time.

Focus on steady progress rather than perfection. Every positive financial decision you make today can strengthen your credit profile and open the door to better financial opportunities tomorrow.

Frequently Asked Questions

What is the highest possible credit score?

Most commonly used scoring models range from 300 to 850, with 850 being the highest possible score.

Does checking my own credit score hurt it?

No. Checking your own score is generally considered a soft inquiry and does not affect your credit score.

How long does it take to improve a credit score?

Minor improvements may appear within a few months, while significant improvements often take six months to a year or more, depending on your credit history.

Is 700 a good credit score?

Yes. A score of 700 generally falls within the Good range and qualifies many borrowers for competitive lending products.

Should I close a credit card I no longer use?

Not necessarily. Closing an older account may reduce your available credit and affect the average age of your accounts. Evaluate annual fees and your overall credit strategy before making a decision.

Can I have more than one credit score?

Yes. Different scoring models and credit bureaus can produce different credit scores based on the information they have available.

What is the fastest way to improve my credit score?

For many people, the quickest improvements come from paying every bill on time, lowering credit card balances, reducing credit utilization, and correcting any errors on their credit reports.