How Credit Scores Are Calculated

How Credit Scores Are Calculated

Have you ever wondered why your credit score changes even when you pay your bills on time? Or why two people with similar incomes can have very different credit scores?

The answer lies in how credit scoring models evaluate your credit history. While the exact formulas used by FICO® and VantageScore® are proprietary, both scoring systems examine many of the same financial behaviors to estimate how likely you are to repay borrowed money.

Understanding these factors allows you to focus on the habits that have the greatest impact on your score.

Quick Overview

| Credit Score Factor | Relative Importance | What It Measures |

|---|---|---|

| Payment History | Very High | Whether you pay bills on time |

| Credit Utilization | High | How much available credit you’re using |

| Length of Credit History | Moderate | How long you’ve managed credit |

| New Credit | Moderate | Recent credit applications and new accounts |

| Credit Mix | Lower | Variety of credit account types |

While no scoring model publicly reveals exact percentages, payment history and credit utilization are generally considered the two most influential factors.

Step 1: Payment History

Payment history is often the most important component of your credit score.

Lenders want evidence that you consistently repay borrowed money as agreed.

Positive payment history includes:

- Credit card payments

- Mortgage payments

- Auto loan payments

- Student loans

- Personal loans

Negative items include:

- Late payments

- Collections

- Charge-offs

- Foreclosures

- Bankruptcies

Even a single payment that becomes 30 days late can lower your score.

Tips to Improve Payment History

- Set up automatic payments.

- Use payment reminders.

- Pay at least the minimum amount due.

- Contact your lender immediately if you’re experiencing financial hardship.

Step 2: Credit Utilization

Credit utilization measures how much of your available revolving credit you’re currently using.

Example

| Credit Limit | Current Balance | Utilization |

| $5,000 | $500 | 10% |

| $5,000 | $2,500 | 50% |

| $5,000 | $4,500 | 90% |

Lower utilization generally indicates responsible credit management.

A commonly recommended goal is to keep utilization below 30%, with many consumers seeing the strongest results below 10%.

Ways to Lower Utilization

- Pay balances before your statement closes.

- Make multiple payments each month.

- Avoid maxing out credit cards.

- Request a credit limit increase if appropriate.

- Spread balances across multiple cards rather than concentrating them on one account.

Step 3: Length of Credit History

The longer you’ve successfully managed credit, the more information lenders have about your financial habits.

This factor considers:

- Age of your oldest account

- Average age of all accounts

- Age of your newest account

Closing older accounts may reduce your available credit and can eventually affect the average age of your accounts.

Best Practices

- Keep older accounts open if they don’t have costly annual fees.

- Avoid opening unnecessary new accounts.

- Build a long history of responsible credit use.

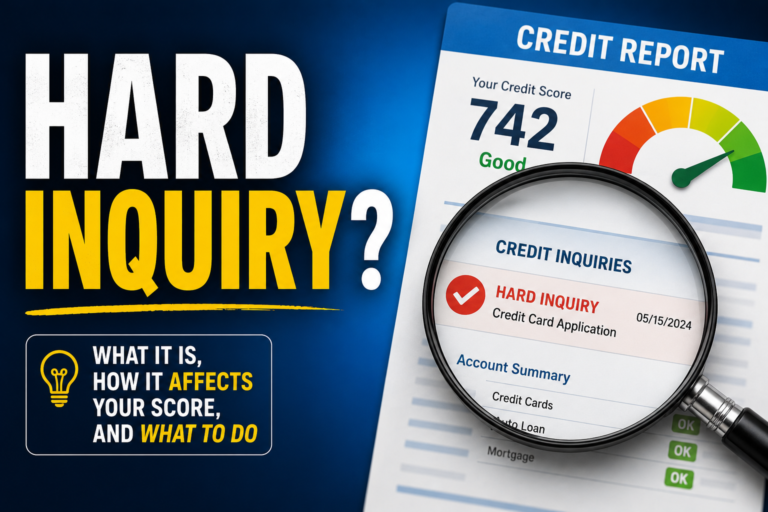

Step 4: New Credit

Applying for credit usually results in a hard inquiry.

Hard inquiries may temporarily lower your score by a few points.

Opening several new accounts within a short period can indicate increased lending risk.

Smart Application Strategy

Instead of applying for multiple credit cards at once:

- Apply only when needed.

- Space applications several months apart.

- Shop for mortgages and auto loans within a focused time period when rate shopping.

Step 5: Credit Mix

Credit mix refers to the different types of credit accounts you manage.

Examples include:

- Credit cards

- Auto loans

- Mortgages

- Student loans

- Personal loans

A healthy mix may slightly benefit your score because it demonstrates experience managing different forms of credit.

However, you should never borrow money simply to improve your credit mix.

Credit Score Simulator

While every credit profile is different, the following examples illustrate how common financial decisions may influence your credit score.

| Financial Action | Typical Impact | When You May See Results |

|---|---|---|

| Pay off a maxed-out credit card | High Positive | 30–60 days |

| Lower utilization below 30% | Moderate to High Positive | 30–60 days |

| Miss a payment | High Negative | After the late payment is reported |

| Open a new credit card | Small Temporary Negative | Immediately after approval |

| Receive a credit limit increase | Moderate Positive if balances remain the same | Next reporting cycle |

| Become an authorized user | Moderate Positive if the account has strong history | 30–60 days |

| Pay off a collection account | Impact varies by scoring model | 30–90 days |

| File for bankruptcy | Severe Negative | Immediate and long lasting |

These examples are general guidelines. Your individual results depend on your complete credit profile and the scoring model being used.

Factors That Do Not Directly Affect Your Credit Score

Many people believe certain personal characteristics influence their score, but these generally do not directly affect credit scoring models.

These include:

- Income

- Occupation

- Education

- Marital status

- Savings account balance

- Checking account balance

- Race

- Gender

While lenders may evaluate some of these factors separately during underwriting, they are not direct components of most credit scoring models.

Common Credit Score Myths

Many misconceptions about credit scores continue to circulate. Believing these myths can lead to poor financial decisions.

Myth: Checking your own credit score hurts your score.

Fact: Checking your own credit score is considered a soft inquiry and generally does not affect your score.

Myth: You should always carry a credit card balance.

Fact: Paying your statement balance in full each month is generally the healthier financial strategy.

Myth: You only have one credit score.

Fact: Most consumers have multiple credit scores because different scoring models and credit bureaus calculate scores differently.

Myth: Closing old credit cards always improves your credit.

Fact: Closing older accounts may reduce available credit and eventually affect the average age of your accounts.

Myth: Income affects your credit score.

Fact: Income is not a direct component of most credit scoring models, although lenders may consider it separately during loan approval.

The Biggest Credit Score Killers

Not all financial mistakes have the same impact. Some can significantly damage your credit score and remain on your credit report for years.

| Credit Event | Typical Impact |

| Bankruptcy | Extremely High |

| Foreclosure | Very High |

| Charge-Off | Very High |

| Collection Account | High |

| 30-Day Late Payment | High |

| Maxed-Out Credit Cards | Moderate to High |

| Multiple Hard Inquiries | Low to Moderate |

| Closing Older Credit Accounts | Moderate depending on your credit profile |

If your goal is to improve your credit score, avoiding these major setbacks is often more important than finding small optimization strategies.

Why Credit Scores Change

Credit scores are dynamic and update as new information is reported.

Common reasons your score may increase include:

- Lower credit card balances

- Additional on-time payments

- Removal of inaccurate information

- Older negative items losing influence over time

Common reasons scores may decrease include:

- Missed payments

- High utilization

- New hard inquiries

- Collection accounts

- Closing credit accounts that significantly reduce available credit

Example Credit Profiles

Profile A

- Always pays on time

- Uses 8% of available credit

- Oldest account is 12 years old

- One recent inquiry

Likely outcome: Strong credit profile.

Profile B

- Missed two payments

- Uses 85% of available credit

- Opened four new accounts recently

Likely outcome: Lower score until those issues improve.

How Lenders Use Credit Scores

Your score helps lenders estimate risk, but it is only one part of the decision.

Many lenders also review:

- Income

- Employment history

- Debt-to-income ratio

- Assets

- Down payment amount

- Overall financial stability

A higher score generally improves your chances of approval and may help you qualify for better interest rates.

What Lenders Actually See

Many people assume lenders can see everything about their finances. In reality, they primarily review information contained in your credit report and the application you submit.

Lenders Typically Review

- Your credit score

- Payment history

- Credit utilization

- Outstanding balances

- Age of your credit accounts

- Types of credit accounts (credit mix)

- Recent hard inquiries

- Total debt

- Debt-to-income ratio (for many loan applications)

- Employment and income information provided during your application

Lenders Generally Do Not See

- Your checking account balance

- Your savings account balance

- Retirement account balances

- Investment account balances

- Your monthly household budget

- Your spending history unless it’s with their own financial institution

Understanding what lenders actually evaluate helps you focus on improving the factors that truly influence lending decisions.

Five Habits That Improve Your Credit Score

- Pay every bill on time.

- Keep utilization below 30%, preferably under 10%.

- Avoid unnecessary credit applications.

- Review your credit reports for errors.

- Maintain older accounts whenever practical.

Key Takeaways

Credit scores are based on patterns, not isolated events.

The strongest credit profiles are typically built by consistently paying bills on time, maintaining low credit utilization, avoiding unnecessary debt, and managing credit responsibly over many years.

Improving your score doesn’t require perfection—it requires consistency.

Before You Apply for New Credit

Whether you’re applying for a mortgage, auto loan, personal loan, or credit card, taking a few steps beforehand may improve your chances of approval and help you qualify for better terms.

Review Your Credit Score

Know where you stand before submitting an application.

Check Your Credit Reports

Review your reports for errors, fraudulent accounts, or outdated information that could affect your approval.

Lower Your Credit Card Balances

Reducing your utilization before applying may strengthen your credit profile.

Avoid New Credit Applications

Multiple hard inquiries within a short period may temporarily lower your score.

Calculate Your Debt-to-Income Ratio

Many lenders evaluate your monthly debt obligations compared to your income.

Compare Multiple Lenders

Interest rates, fees, and qualification requirements vary, so shopping around can save money over the life of a loan.

Gather Your Financial Documents

Having income verification, identification, and other required documents ready can make the application process smoother and faster.

Preparing before you apply can improve both your approval odds and the interest rate you receive.

Frequently Asked Questions

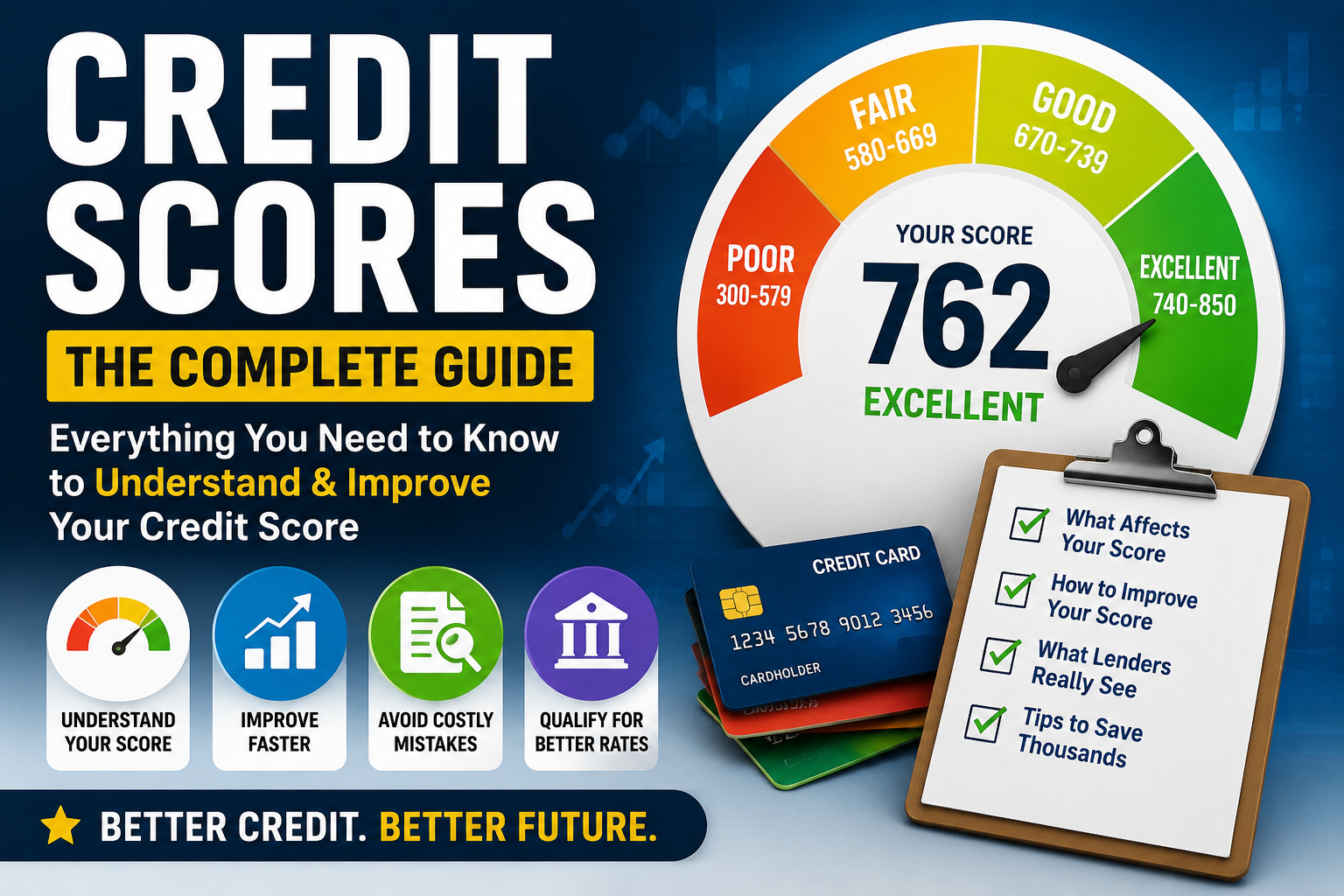

Are credit scores calculated the same by every company?

No. Different scoring models, such as FICO and VantageScore, use different formulas, so your scores may vary.

Which factor affects my credit score the most?

Payment history is generally considered the most influential factor, followed closely by credit utilization.

How often are credit scores updated?

Your score may change whenever lenders report new account information to the credit bureaus, which is often monthly.

Does paying off a credit card automatically increase my credit score?

It often helps by lowering your credit utilization, but the exact impact depends on your overall credit profile.

Can I improve my credit score quickly?

Some people see improvements within a few months by lowering balances and making all payments on time, but long-term improvement comes from consistent financial habits.